What is it?

At its core, disability insurance provides a tax-free monthly benefit if an unexpected illness or accident prevents you from working. When your income stops, your bills don’t. This coverage acts as a critical safety net, allowing you to meet your financial obligations and maintain your family’s lifestyle during a difficult time.

Because every career is unique, Paradigm Insurance Inc. offers a comprehensive catalogue of customizable disability products. We do the heavy lifting to tailor your policy, giving you control over key variables:

Benefit Periods: The length of time you receive payments, ranging from short-term relief to long-term coverage.

Benefit Amounts: Your tax-free monthly income, ranging from hundreds to tens of thousands of dollars to accurately replace your take-home pay.

Occupational Customization: Specialized products built specifically for professions of all types.

How does it work?

It is standard practice to insure our homes and vehicles, yet many of us overlook our most valuable asset: our ability to earn an income. Over a lifetime, your earning potential is immense. For example, a 30-year-old making $70,000 a year will earn well over $3.8 million before retirement. Protecting this future income is a critical step in securing your financial well-being.

Disability insurance replaces a percentage of that income if an illness or accident keeps you from working. At Paradigm, we simplify the process by calculating exactly how much coverage you need. A key rule we navigate for you is the “all-source maximum"—an industry standard ensuring your total disability income (from all sources combined) does not exceed 85% of your pre-disability earnings.

To design an efficient, tailored strategy, we help you define three crucial policy features:

Employment Classification: Matching the policy to the specifics of your job.

Waiting Period: How soon your tax-free payments begin after an injury or illness.

Benefit Period: How long those payments will last.

The above variables along with:

age

occupation

health history

smoker status

will determine your disability rates.

Each disability insurer has pre-assigned nearly all occupations, spanning from axe throwing company owner to zoo therapist, with a classification code. This code represents the risk associated with any particular occupation and consequently contributes to determining the premium. The classification codes vary slightly from insurer to insurer; however, the following is a rough breakdown of how the system works:

4S

This classification offers preferred rates to select professionals and executives. To qualify for this classification, one must meet a number of criteria which, in the eyes of the insurer, lower the likelihood of experiencing a disability. Most commonly, individuals in the medical field (excluding emergency medicine), lawyers, business owners, and other white-collar workers who meet specific criteria occupy this class.

4A

The 4A classification houses select business professionals who do not meet the salary and experience thresholds to upgrade to a 4S classification. Examples of occupations which often receive the 4A classification are architects, PhD scientists, teachers, and financial professionals.

3A

Primarily office workers with light sales duties and no manual labour responsibilities occupy the 3A classification. So, we often see office managers, office workers, and scientists with an Undergraduate of Master’s degree be assigned the 3A classification.

2A

The 2A classification is similar to the 3A and often includes sales professionals and other skilled workers who are often travelling from place to place during working hours. Occupations such as locksmiths, insurance adjusters, home inspectors, and reporters are commonly classified as 2A.

A

The A classification contains certain industry and trades workers. Receiving the A classification is possible when particular criteria relating to working conditions (i.e. proximity to chemicals, heavy equipment, etc.) are met. Mechanics, bus drivers, and electricians are examples of occupations which often carry the A classification.

B

The B class is the final designation. Occupations which receive this classification often require significant physical exertion or have a high-risk of accident. Additionally, occupations with a history of employment instability may receive the B classification. Some examples of occupations which commonly receive the B classification are as follows: disk jockeys, blacksmiths, concrete workers, roofers, and heavy-duty mechanics.

Once we have determined your occupation class and calculated the right coverage amount, we guide you through three simple steps to finalize your strategy:

The waiting (or elimination) period is the time between when you become disabled and when your tax-free payments begin. Your choice here depends entirely on your financial comfort and savings. Opting for a longer waiting period—traditionally 30, 60, 90, or 120 days—results in a lower monthly premium. We help you find the perfect balance between upfront affordability and timely financial relief.

This determines exactly how long your payments will last if you cannot return to work. Many clients choose an “Age-65" benefit period, ensuring their income is protected right up to standard retirement age. Alternatively, 2-year and 5-year benefit periods offer practical, cost-effective options for shorter-term protection.

Once an appropriate monthly benefit amount is calculated, the proper employment code is derived, and the waiting and benefit periods are determined, the next step is to apply for the coverage.

At Paradigm, we believe in a pressure-free experience. Every application is strictly no-obligation, meaning you can cancel the process at any time—even after the policy is approved—with absolutely no fees payable.

We also value your time. For clients between the ages of 18 and 50 applying for less than $6,000 a month in coverage, we can often use accelerated underwriting. This means your policy can frequently be approved without the need for biometrics like blood work, urine tests, or physical exams. Once approved, you can enjoy the peace of mind that comes from knowing your hard-earned income is secure.

Who benefits from it?

Individuals of any age and background can experience an accident or illness which restricts their ability to work. Listed below are a couple of real-life claim examples:

Age 36, Chronic Fatigue,

$881,373 disability benefit paid from

2001 to 2018

age 29, back injury,

$536,036 disability benefit paid from

2003 to 2018

age 32, brain aneurysm,

$272,422 disability benefit paid from

2005 to 2018

age 37, major depression,

$637,846 paid from 1998 - 2018

Who can apply?

If you are working and between the ages of 18 and 60, you are eligible to apply for disability coverage.

Many clients come to us assuming their employer’s group benefits are enough. While workplace coverage is a great starting point, it often has hidden limitations—such as capping your monthly payout or ending entirely the moment you change jobs. A privately owned policy ensures your protection stays with you, giving you permanent control and peace of mind regardless of where your career takes you.

What are the odds of an accident happening?

An unexpected health event can strike anyone at any time. In fact, 1 in 4 Canadians will experience a disability lasting at least 90 days before they reach age 65. For those facing an absence longer than six months, the average duration of recovery is nearly six years.

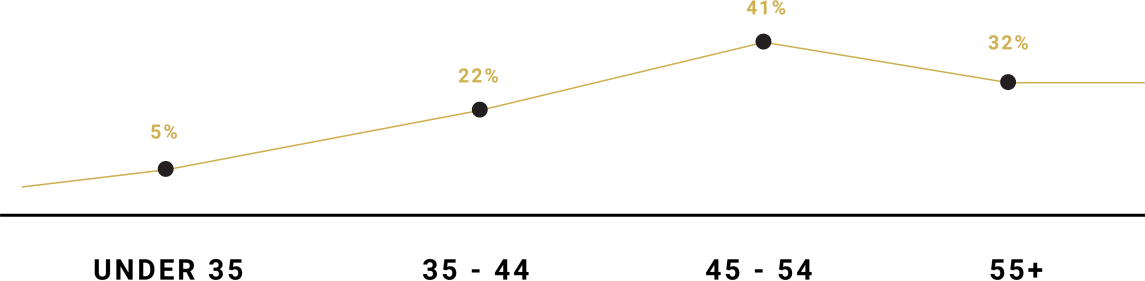

While the risk naturally increases as we get older, no age group is immune. Here is a general breakdown of disability claims by age:

What disabilities are covered?

The Government’s Canadian Pension Plan (CPP) and Worker’s Compensation benefits certainly help those who can utilize them. However, the CPP benefit only pays out if the disability is such that one cannot perform any job, not just their chosen profession. Furthermore, Worker’s Compensation only results in a benefit being paid if the disability is caused by a workplace incident.

Our disability products result in a benefit regardless of the cause of one’s disability. The list below depicts various disabilities and the percentage of claims each are responsible for: